Big news in Tahoe this week: A major legal decision has overturned South Lake Tahoe’s short-term rental ban (see the article below), ruling it unconstitutional and opening the door for non-resident homeowners to once again operate vacation rentals. Meanwhile, in positive economic news, interest rates have fallen to their lowest levels this year., creating a significant shift in the market. And if that weren’t enough, Tahoe just got buried in fresh snow, with some areas seeing over two feet overnight—one of the biggest single-day snowfalls in years! Hope to see you on the slopes!

Mortgage Rates Hit Lowest Point So Far This Year

Mortgage Rates Hit Lowest Point So Far This Year After a prolonged period of elevated mortgage rates, we’re finally seeing a meaningful decline—an encouraging shift for those of us in the investment space. While rates remain higher than the historic lows of past years, this recent movement presents an opportunity to reassess financing strategies and potential acquisitions. As seasoned investors, we know that market conditions are always evolving, and staying ahead of these shifts is key to making informed, strategic decisions.

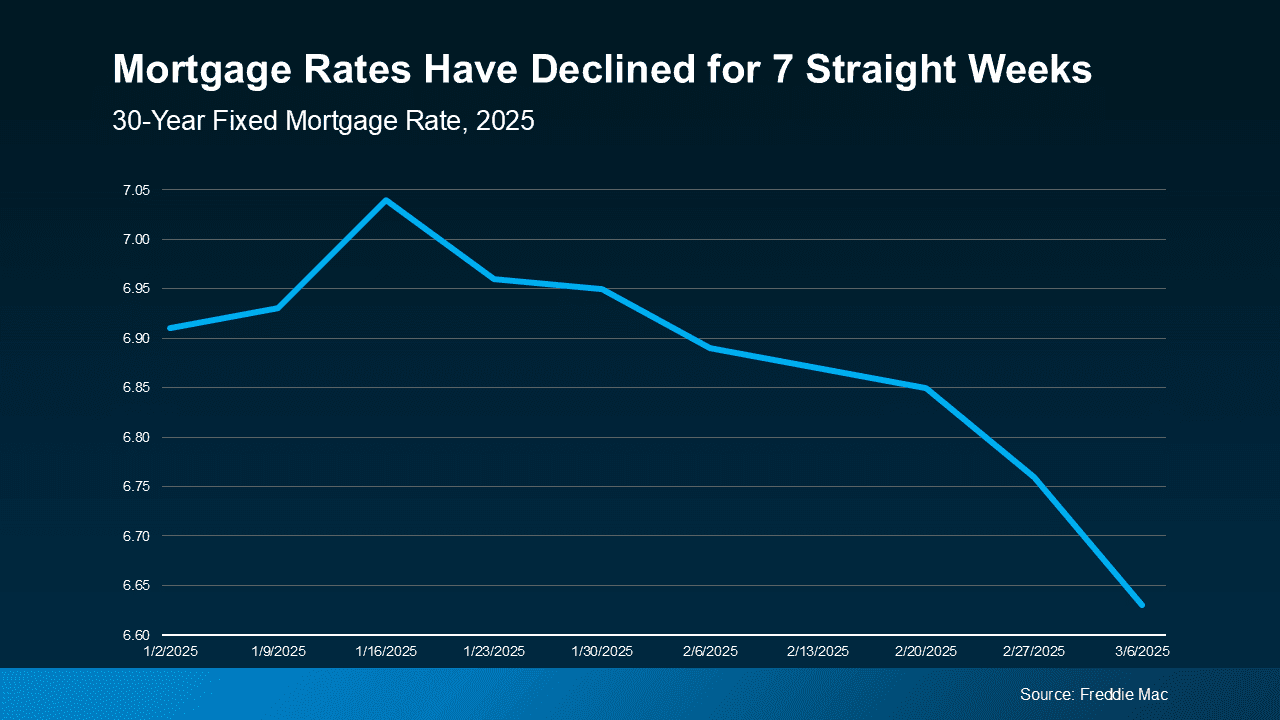

Current Mortgage Rates & Market Trends Mortgage rates had been declining for seven consecutive weeks but have recently edged slightly higher, with the 30-year fixed rate now averaging 6.65%. While this marks a small increase from recent lows, it still represents a significant shift from the peaks above 7% earlier this year.

Other key rates include:

- 20-year fixed mortgage: 6.40%

- 15-year fixed mortgage: 5.95%

- 5/1 Adjustable-Rate Mortgage (ARM): 6.50%

- 7/1 ARM: 6.45%

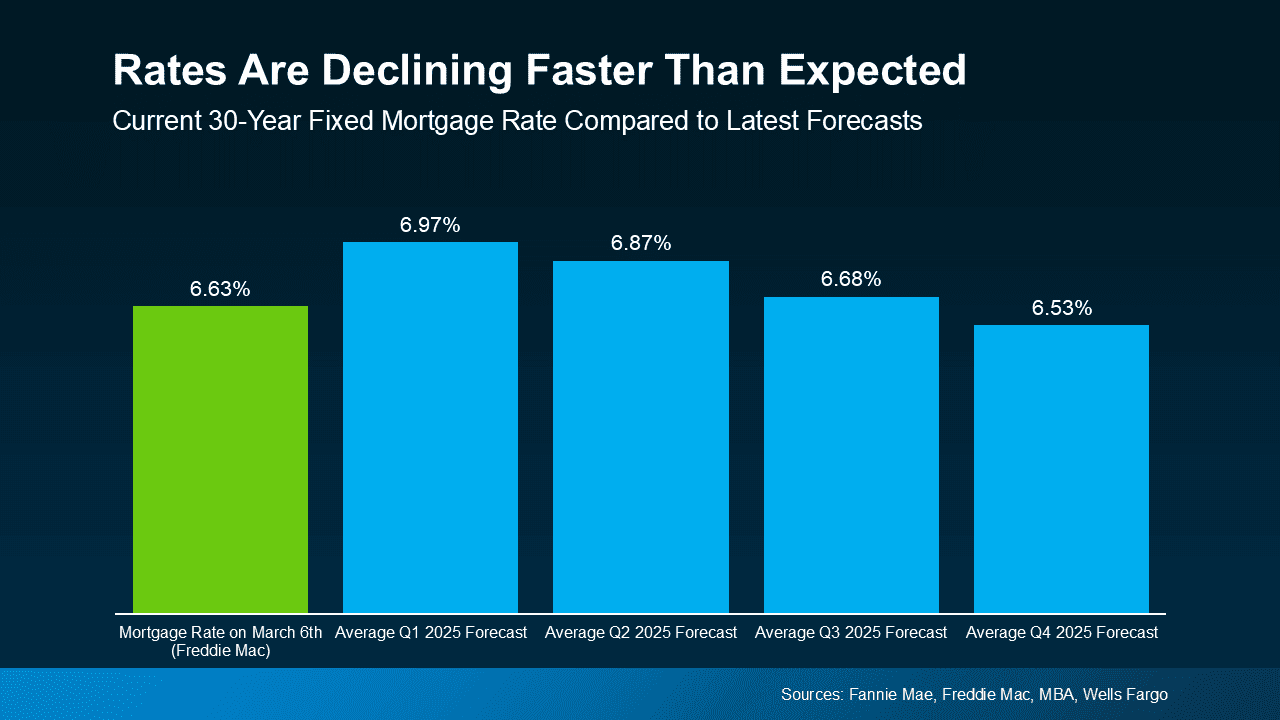

Despite this recent slight increase, mortgage rates remain lower than many forecasts projected for this point in the year, presenting an opportunity for strategic financing adjustments.

Why Are Rates Fluctuating?

A combination of economic factors has contributed to recent shifts in mortgage rates, including:

- Market Volatility – Fluctuations in the financial markets, partly influenced by U.S. trade policies and global economic concerns, continue to impact bond yields, which directly influence mortgage rates.

- Federal Reserve Policies – The Fed’s cautious approach to interest rates has played a role in keeping mortgage rates relatively stable, but long-term direction remains uncertain.

- Shifting Buyer Activity – With rates lower than they were at their peak, buyer demand has increased, leading to a 5% rise in purchase applications compared to last year.

What Lower Rates Mean for Buying Power

The recent mortgage rate trends are already impacting the real estate market. Last week, mortgage applications jumped 11.2% from the previous week and 31% compared to a year earlier, according to the Mortgage Bankers Association. And a measure of home loan refinancing applications surged 16%, the MBA said.

Locally, the median list price of a home was $2.2 million in January 2025, reflecting a 4.3% increase compared to 2024.

To compare how lower mortgage rates directly impact financing costs, consider the following:

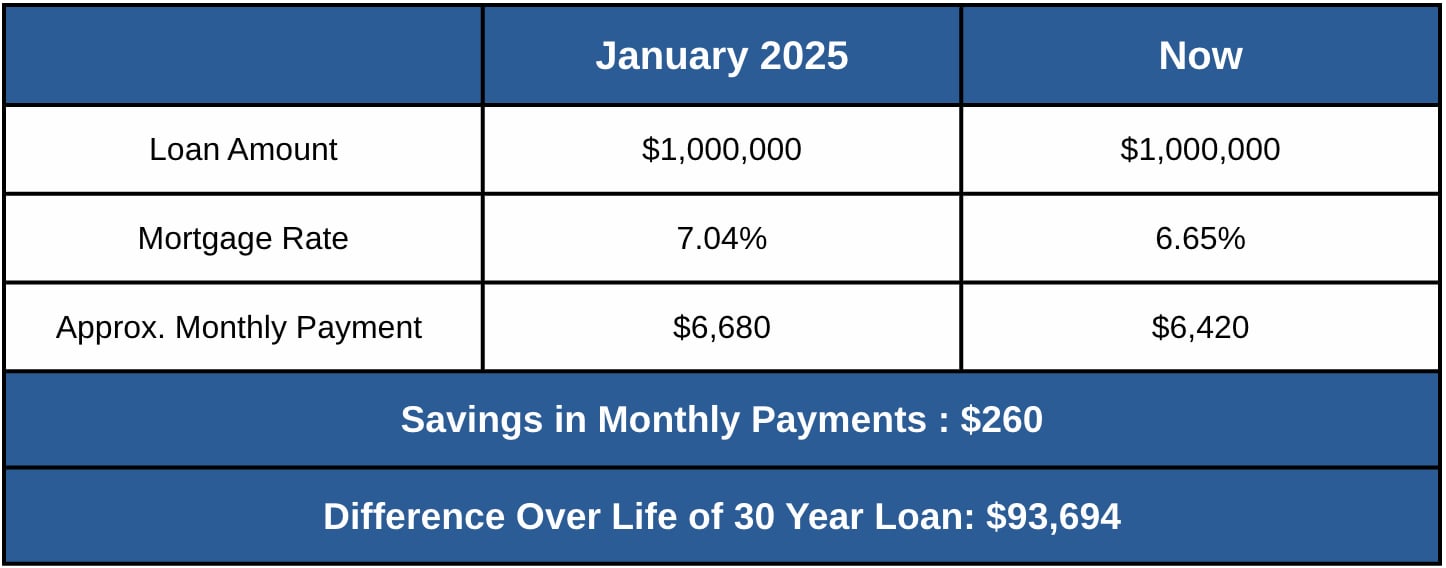

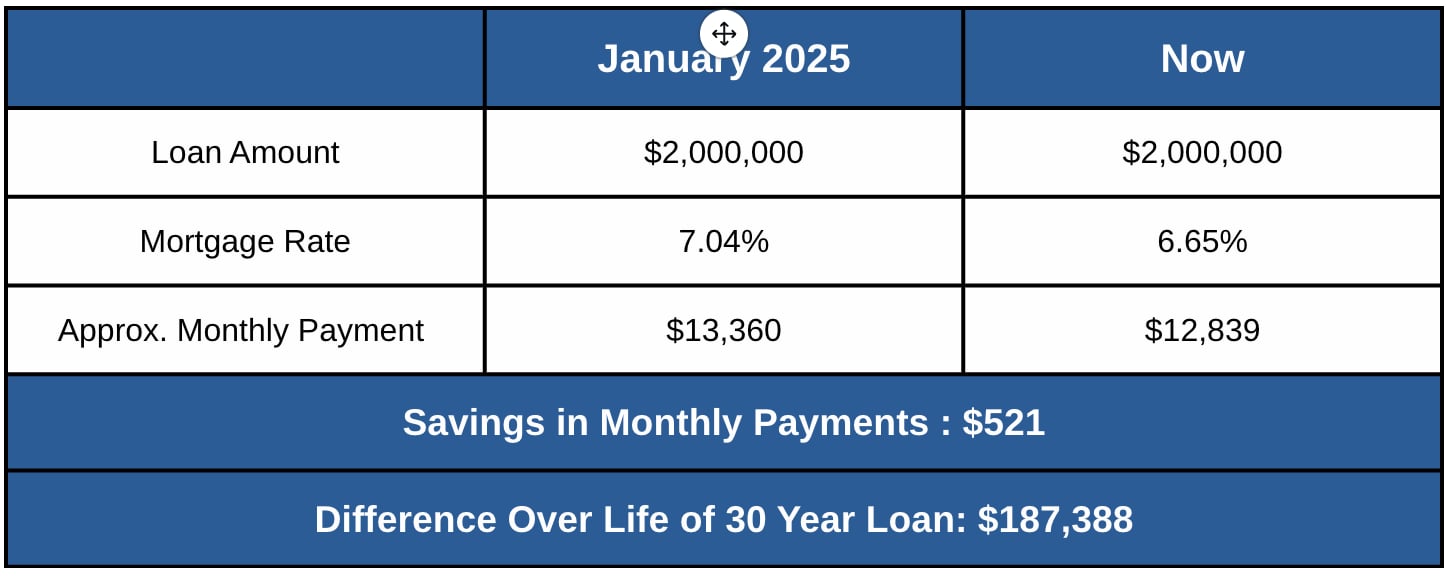

- Monthly Payment Reduction: For a $1 million loan, the monthly payment at 7.04% (the peak rate from mid-January) was approximately $6,690. At 6.65%, that payment drops to about $6,520—a difference of over $170 per month.

- Total Savings Over Loan Term: This reduction equates to nearly $60,000 in savings over the life of a 30-year loan.

While these savings may not seem dramatic on a monthly basis, they add up significantly over time, improving cash flow and investment returns (see below):

Looking Ahead

While rates have increased slightly from their recent lows, they remain below the peaks seen earlier this year. The Mortgage Bankers Association anticipates that rates will hover in the mid-to-high 6% range for the first half of 2025, though economic uncertainty—including inflation and trade policies—could introduce volatility.

For those considering acquisitions or refinancing, this current window may still provide an opportunity to secure more favorable financing before conditions shift again. Timing the market perfectly is impossible, but staying informed and adapting to real-time data allows us to make the best strategic moves for our portfolios.