How the Economy Impacts Mortgage Rates

Most potential buyers and sellers have been on the sidelines waiting and paying close attention to mortgage rates and speculating about future trends. A significant factor influencing mortgage rates is the Federal Funds Rate, which affects the cost of interbank borrowing. Although the Federal Reserve (the Fed) does not directly set mortgage rates, it controls the Federal Funds Rate, creating a close relationship between the two. Consequently, any reduction in the Federal Funds Rate by the Fed exerts downward pressure on mortgage rates.

The Fed's upcoming meeting will involve evaluating three critical metrics: the rate of inflation, the number of jobs added to the economy, and the unemployment rate. The latest data on these metrics are as follows:

These metrics will guide the Fed's actions, potentially impacting future mortgage rates.

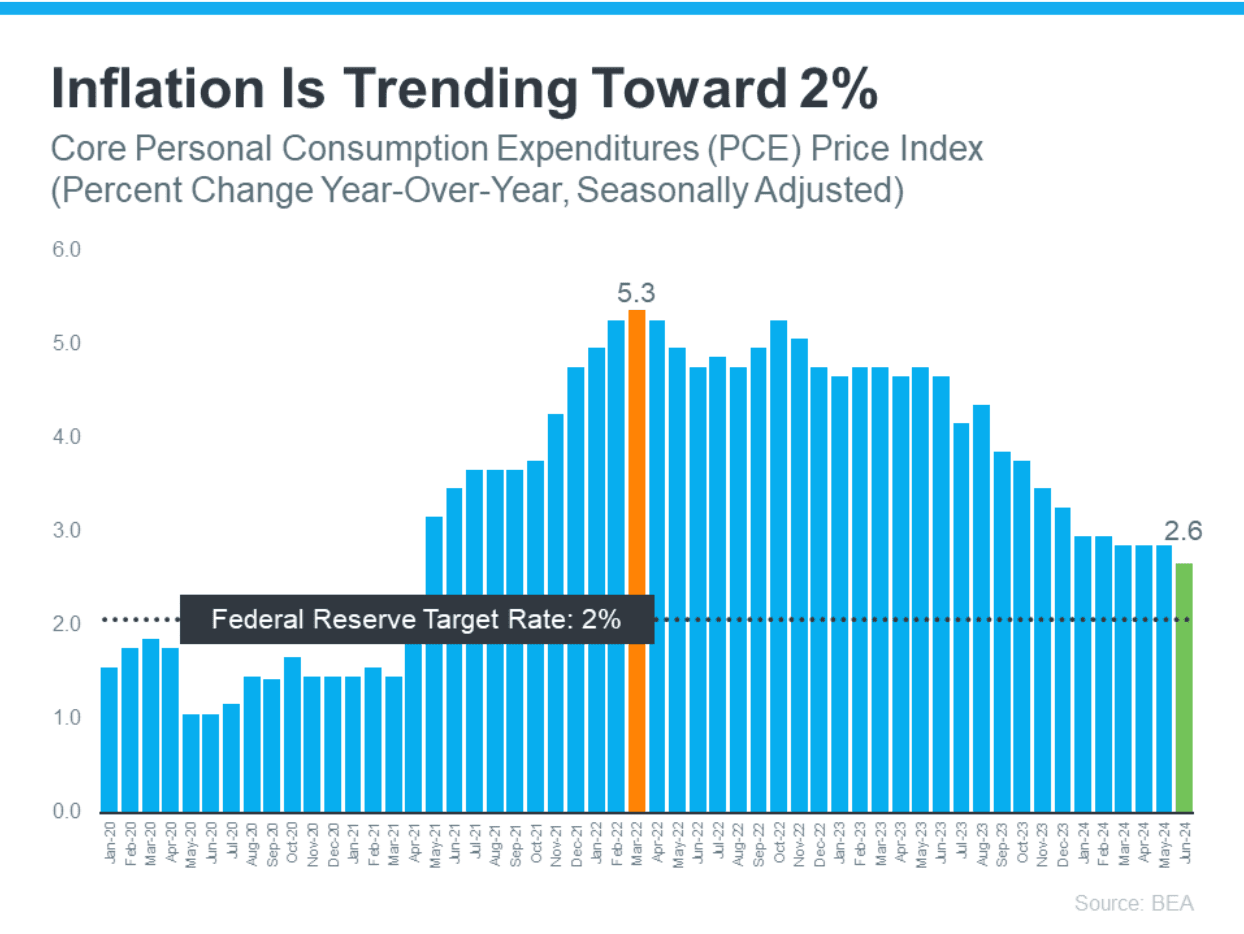

The Fed has stated its goal is to get the rate of inflation back down to 2%. Right now, it’s still higher than that, but moving in the right direction (see graph below):

The Federal Reserve closely monitors the monthly creation of new jobs. Consistent moderation in job growth is a key indicator the Fed seeks before making any adjustments to the Federal Funds Rate. A decline in job creation suggests that the economy remains robust but is beginning to cool, aligning with the Fed's objectives. Recent data supports this trend. According to Inman:

". . . the Bureau of Labor Statistics reported that employers added fewer jobs in April and May than previously thought and that hiring by private companies was sluggish in June."

This data indicates a slowdown in job additions, suggesting a deceleration in the economy after a prolonged period of overheating. This trend is viewed positively by the Federal Reserve.

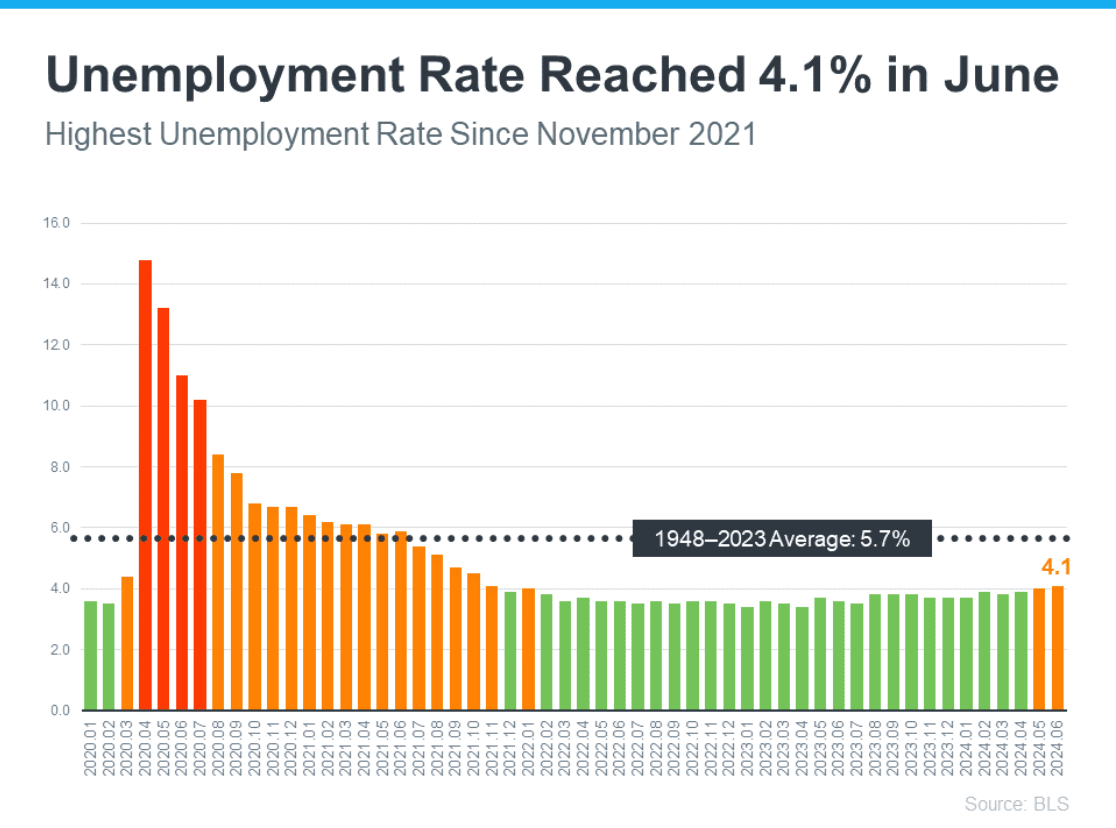

The unemployment rate represents the percentage of individuals seeking employment but unable to find jobs. A low unemployment rate indicates a high level of employment among Americans. However, it can also contribute to higher inflation, as increased employment typically leads to higher spending, driving up prices. Currently, the unemployment rate remains low but has shown a gradual increase over recent months. (see graph below).

It may seem harsh, but a consistently rising unemployment rate is something the Fed needs to see before deciding to cut the Federal Funds Rate. That’s because a higher unemployment rate would mean reduced spending, and that would help get inflation back under control.

While mortgage rates are going to continue to be volatile in the days and months ahead, these are signs the economy is headed in the direction the Fed wants to see. But even with that, it’s unlikely they'll cut the Federal Funds Rate when they meet next week. Jerome Powell, Chair of the Federal Reserve, recently said:

“We want to be more confident that inflation is moving sustainably down toward 2% before we start the process of reducing or loosening policy.”

We’re seeing the first signs now, but they need more data and more time to feel confident that this is a consistent trend. Assuming that direction continues, according to the CME FedWatch Tool, experts say there’s a projected 96.1% chance the Fed will lower the Federal Funds Rate at their September meeting.

Of course, the timing of when the Fed takes action could change because of new economic reports, world events, and other factors. The market has been consistently picking up and hopefully will continue to do so as we head into the fall, typically our busiest time of the year.

Activities, Events, Live Music

The Science of Scaling

Get In Touch