What to Expect from the Housing Market in the Second Half of 2025

This week, we're shifting focus to what the second half of 2025 might bring—based on the latest forecasts and expert projections.

Looking Ahead: What the Data Tells Us About the Housing Market for the Rest of 2025

If you’ve been keeping an eye on housing headlines lately, you’ve probably seen a mix of predictions—some cautiously optimistic, others alarmist. And depending on the week, it can feel like we’re either on the verge of a price surge or a long-awaited correction. But as we move through the second half of 2025, most experts aren’t forecasting either extreme.

Instead, the data points to something far less dramatic: a market that’s finding its footing.

Over the past few weeks, I’ve reviewed projections from Fannie Mae, the Mortgage Bankers Association (MBA), Wells Fargo, and several national housing analysts. Here’s what the numbers are showing—and what it may mean for buyers, sellers, and those still waiting for a clear signal.

Statement from NAR Chief Economist:

“Nationally, sales decreased in June by 2.7% month over month. However, there was no change year over year. There are 1.53 million homes on the market, which equates to 4.7 months’ supply and is a 15% increase from a year ago. Median home price increased 2% to $435,300—a record high ($2,450,000 locally).

Due to the continued growth of home prices over the past five years, the average homeowner’s wealth has expanded by nearly $150,000. Multiple years of undersupply are driving the record-high home prices. High mortgage rates are making it harder for first-time homebuyers to enter the market. Only 30% of sales were to first-time homebuyers.

If rates decline in the second half of the year, expect home sales to increase due to strong income growth, healthy inventory, and a record-high number of jobs.”

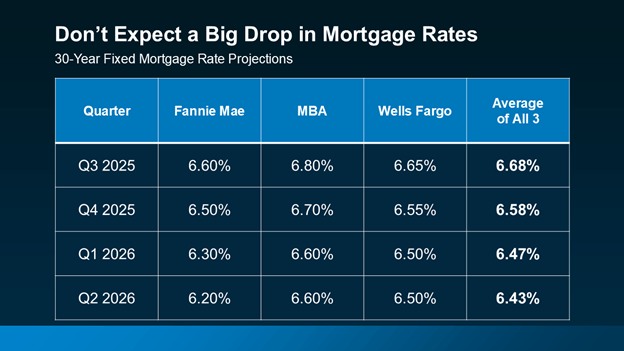

Mortgage Rates: Mid-6% Is the New Normal—for Now

One of the most common questions I hear is: “Are rates coming down soon?” And it’s a fair question—especially for buyers hoping to time their move with better financing. But the sharp rate drop many expected hasn’t materialized, and projections now suggest a more modest path forward.

Forecasts from Fannie Mae, MBA, and Wells Fargo all point to rates hovering in the mid-6% range through the rest of 2025 and into early 2026. The average projection for Q3 is 6.68%, softening slightly to 6.43% by Q2 of next year.

The key takeaway is that rates are expected to gradually decline, but not dramatically. For those waiting for a return to the 4–5% range, that may not be realistic anytime soon.

What this means in practice: the market is adjusting. Buyers are recalibrating expectations, and many are realizing that waiting indefinitely for 5% financing may not be the most effective strategy—especially if prices continue to edge upward.

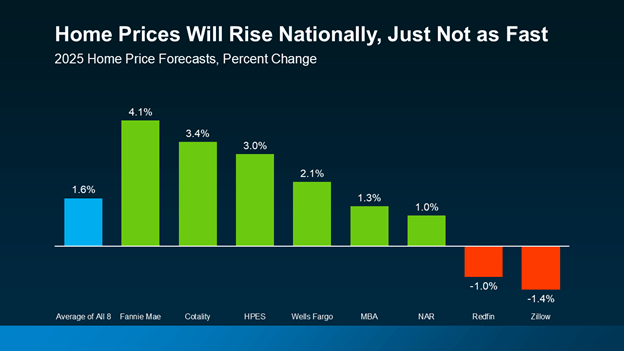

Home Prices: Slowing Appreciation, Not Decline

Another area of confusion is home values. Some buyers are waiting for a drop; others are wondering if they’ve missed the window. But so far, most forecasts point to continued growth, just at a much slower and more sustainable pace.

The average of eight major home price forecasts shows 1.6% appreciation in 2025, with a range from Fannie Mae’s optimistic 4.1% to Redfin and Zillow’s modest projected declines.

This kind of spread reflects regional variation more than volatility. In places where affordability is stretched or pandemic-era gains were steep, there may be a pullback. But nationally—and especially in lifestyle-driven second-home markets like Tahoe—the fundamentals still support stable pricing.

Inventory Is Climbing, but Still Tight by Historical Standards

National inventory has grown meaningfully over the past 12 months, with Realtor.com reporting a 39% year-over-year increase in active listings. But supply still remains more than 30% below pre-pandemic levels in many areas.

Here on the East Shore, we are seeing more properties come to market—but selection remains limited in certain segments. Well-located homes with views, privacy, or lake access still generate interest. Price reductions are happening, but mostly on listings that started too high or lack compelling features.

Nationally, homes are spending an average of 45 days on market, which is longer than during the peak frenzy, but similar to pre-2020 norms. We’re also seeing more seller concessions and financing incentives, especially for properties that need updating or sit in less competitive areas.

Cash Is Still King

Across the country, cash purchases now make up 32% of all home sales, according to the National Association of Realtors—up from 24% in 2019. In Tahoe, that number remains much higher at 54%. In the luxury segment and especially for second homes, financing decisions are often strategic rather than necessary.

This continues to create a two-track market. Buyers reliant on financing are more cautious and rate-sensitive, while cash buyers are moving more quickly when the right opportunity arises.

Buyer and Seller Behavior Has Evolved

The biggest shift isn’t in prices or interest rates—it’s in mindset.

East Shore: Still Holding Steady

Our local market doesn’t always mirror national trends. While some urban and first-time buyer markets are facing pressure from higher rates and affordability constraints, the East Shore remains relatively insulated.

Yes, the pace has slowed. Buyers are taking longer to make decisions, and showings aren’t quite as frequent. But pricing has remained stable, especially in neighborhoods with long-term demand and limited turnover. Properties that check all the boxes—views, beach access, low maintenance, or rental flexibility—continue to sell well.

And importantly, inventory remains limited relative to the size and demand of the market. This is one of the key reasons we’re not seeing downward pressure on prices.

Final Thoughts: What This Market Rewards

We’re in a fundamentally different place than we were two or three years ago. The frenzied pace is gone—but so is the uncertainty of early 2023. In many ways, this is a healthier, more balanced market—especially for buyers and sellers who are prepared and well-informed.

A few things to keep in mind:

Expect mid-6% mortgage rates through at least mid-2026.

If that’s a dealbreaker, it's best to plan accordingly now rather than wait for a rate that may not return anytime soon.

Prices are not falling at the national level.

They’re simply appreciating more slowly, and in some cases, adjusting slightly in overheated areas. Locally, pricing remains resilient.

Inventory is improving, but competition for the best properties is still real.

Being ready to act quickly when something great hits the market still matters.

Strategy matters more than timing.

There may not be a “perfect” time to buy or sell—but having the right strategy in place makes all the difference.

Get In Touch